Behind every great business is a strong financial model that correctly defines the nature of long-term manufacturing investments and operational expenses on a day-to-day basis. On the other hand, where cost elements are misunderstood or merged, the ripple effects are drastic:ruined pricing schemes, defective budgets, and lost competitive advantage.

Therefore, for both manufacturing and financial managers, understanding the difference between manufacturing cost and production cost is like fine-tuning a precision instrument. Every dial and reading has to be precise to result in maximum performance.

Why Does This Matter?

Total manufacturing cost-with its broad focus on raw materials, labor, and overhead-represents the backbone of the production lifecycle. In contrast, production cost zeroes in on the immediate operational expenditures that keep the production line humming. Recognizing and acting upon these distinctions is pivotal for devising pricing strategies that recover costs and generate healthy profit margins.

In this comprehensive discussion, we’ll explore the fundamental components of manufacturing and production costs, expose common misconceptions that obscure their true impact, and provide actionable strategies for harnessing these insights.

Manufacturing Cost vs Production Cost: The Basics

Understanding the different cost elements in manufacturing can reveal clear paths to better efficiency and profitability. However, even though these terms are often used interchangeably, they actually have distinct meanings with significant strategic impacts.

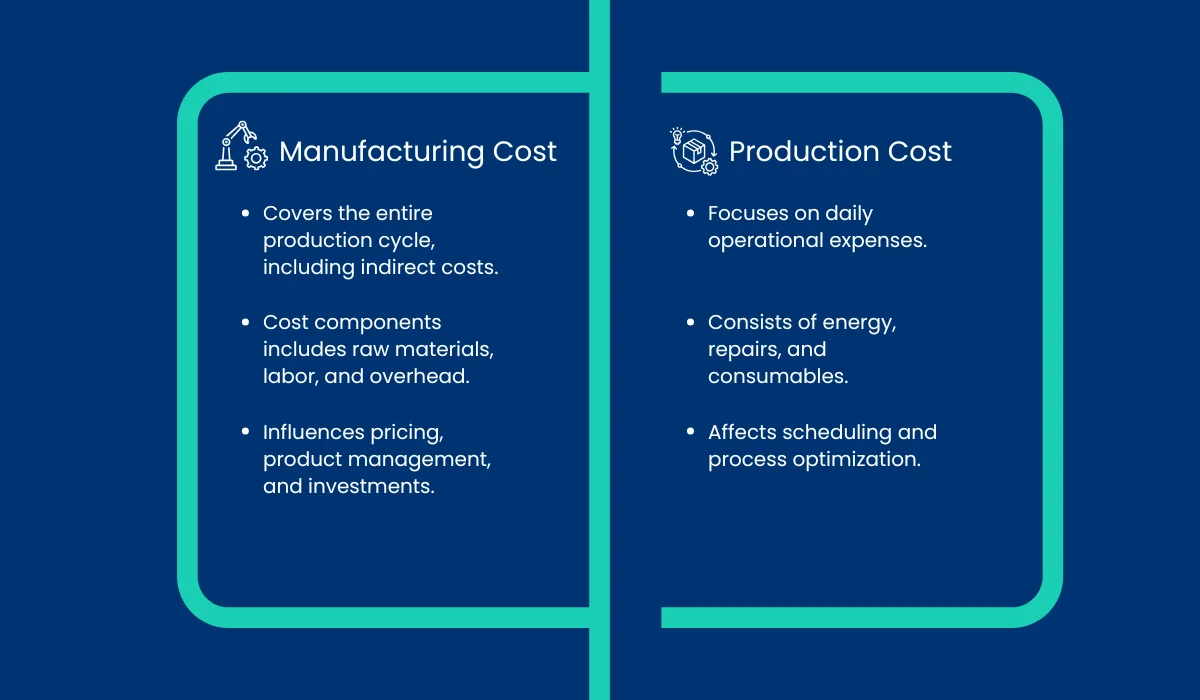

What is Manufacturing Cost?

Manufacturing cost covers all the expenses involved in making a finished product. It mainly consists of three key components:

- Raw Materials: The foundation of every manufactured product, raw materials account for the physical inputs necessary for production. Their cost is not merely the purchase price but also includes storage, handling, and quality control expenses.

- Direct Labor: It represents the wages and benefits of workers directly involved in production. Unlike indirect expenses, these costs are closely tied to the actual output and vary depending on production volume.

- Manufacturing Overhead: Manufacturing overhead can be tricky to break down because it includes indirect costs like utilities, equipment depreciation, and maintenance. Even though these expenses can’t be linked to a single product, they are essential for keeping the production environment running smoothly.

By integrating these components, manufacturing costs offer a panoramic view of the entire production lifecycle. They do more than just add up figures. They reflect the inherent complexities of production planning, resource allocation, and capacity management.

Understanding manufacturing costs is essential for plant managers and CFOs to develop long-term strategies that align with overall business objectives.

What is the Cost of Production?

While manufacturing cost provides a holistic picture, production cost narrows the focus to the daily expenses that keep operations fluid and efficient. Production costs typically includes:

- Operational Expenses: These are the day-to-day expenditures directly linked to the production process. They encompass labor, materials, consumables, energy costs, and minor repairs that maintain operational continuity.

- Process Optimization Investments: In an era of lean manufacturing and continuous improvement, production cost is now also a factor in expenditures on process innovation. Whether through automation upgrades or quality improvement initiatives, these investments are designed to streamline workflows and enhance productivity.

Production cost, therefore, serves as a critical metric for operational decision-making. It provides production and operations managers with immediate insights into efficiency, helping them quickly adjust processes and allocate resources. In contrast to the broader scope of manufacturing cost, production cost is more fluid and responsive, adapting to the dynamic nature of day-to-day operations.

Also Read: A Beginner’s Guide to Decoding Product Cost

What is the Difference Between Production Cost and Manufacturing Cost?

Understanding different types of costs is crucial in the manufacturing industry. Here is the head-to-head comparison of cost of production and manufacturing that reveals the overlapping elements and the unique features that define them.

1. Scope

Manufacturing Cost: Encompasses the entire production lifecycle, from raw material acquisition to final product assembly, including indirect costs.

Production Cost: Focuses on the immediate operational expenses that drive day-to-day production efficiency.

2. Cost Components

Manufacturing Cost: Raw materials, direct labor, and manufacturing overhead.

Production Cost: Direct operational expenses such as energy, minor repairs, and process-related consumables.

3. Time Horizon

Manufacturing Cost: Often used for long-term financial planning and capacity analysis.

Production Cost: More relevant for short-term operational adjustments and efficiency evaluations.

4. Strategic Application

Manufacturing Cost: Influences pricing strategies, product lifecycle management, and investment decisions.

Production Cost: Directly impacts scheduling, process optimization, and immediate cost control measures.

Common Misconceptions

One of the most prevalent misconceptions is that manufacturing cost and production cost are interchangeable terms. This oversimplification can lead to significant strategic missteps such as:

- Pricing Mistakes: Blending these costs can result in charging prices that do not completely cover the cost of production, which can reduce profit margins.

- Budgeting Problems: Without proper boundary, hidden overhead expenses could be overlooked, leading to budget deficits at peak periods.

- Competitive Setback: A loose cost picture can delay a company’s reaction to changing markets.

The Financial Impact: Beyond the Numbers

Translating detailed cost analysis into financial success is where theory meets practice. The ability to effectively break down manufacturing and production costs can redefine profit margins, recalibrate pricing strategies, and underpin cost management best practices.

Profit Margins and Pricing Strategy

Accurate cost measurement is the linchpin of an effective pricing strategy. By clearly delineating manufacturing cost from production cost, companies can ensure that every product’s price reflects its true cost base, paving the way for sustainable profit margins.

Enhanced Pricing Accuracy

When every cost component is meticulously accounted for, businesses can set prices that recover expenses and offer competitive advantages in the market. For example, a mid-sized manufacturing firm recently revisited its cost structure and identified a significant underestimation of overhead expenses. This newfound clarity enabled the firm to adjust its product prices, resulting in a more robust margin without sacrificing market share.

The Strategic Payoff

Ultimately, the clear distinction between manufacturing and production costs yields a strategic payoff extending far beyond the balance sheet. It empowers leaders to:

- Fine-Tune Budget Allocations: With a clear view of where money is spent, CFOs and cost managers can better align budgets with actual needs, ensuring that every dollar brings maximum impact.

- Optimize Resource Utilization: A detailed understanding of cost drivers allows for more effective resource allocation, reducing waste and enhancing overall efficiency.

- Strengthen Competitive Positioning: In an era where precision and agility are paramount, companies that master cost management can swiftly adapt to market changes, pricing their products to capture both value and market share.

- Drive Future Growth: Beyond immediate financial gains, clear cost insights pave the way for strategic investments in technology and innovation. By channeling savings into process improvements, organizations set themselves up for sustained growth in a rapidly evolving industrial landscape.

Conclusion

Learning the differences between manufacturing and production costs is more than a bookkeeping exercise-it’s a strategic imperative. This understanding is vital for manufacturing executives, financial managers, and operations leaders in the quest for operational excellence and competitive advantage. Through detailed cost analysis, businesses gain clarity over their financial landscape and unlock new avenues for growth, innovation, and profitability.

The future belongs to those who can transform complex cost data into actionable strategies. By embracing software of cost optimization, lean methodologies, and cross-functional collaboration, companies can ensure that their pricing, budgeting, and resource allocation are firmly rooted in reality. This level of precision, coupled with a forward-thinking approach, fortifies profit margins and drives strategic growth in an increasingly dynamic market.